More expertise by

Organization

Transaction Support

Restructuring

Implementation Support

Digital Solutions

Change Management

Sustainability

A corporate sustainability strategy enables housing providers to engage with tenants, communities, public authorities and stakeholders.

A corporate sustainability strategy shows how housing providers are positively addressing the Net-Zero Carbon agenda. The strategy also enables housing providers to engage with tenants, communities, public authorities, and stakeholders.

A sustainability strategy is a long-term multi business cycle journey that requires embedding in a corporate strategy and reflected in business operations. Housing providers are faced with the challenge of reconciling internal strategic objectives (e.g., affordability, new house building) with external policy, legal (e.g., climate laws) and regulatory requirements (e.g., governance). The goal is to develop a framework with which sustainability goals can be operationalised, prioritised, placed on a timeline and where any conflicting goals can be resolved.

The Corporate Sustainability Reporting Directive (CSRD) is ready to revolutionise sustainability reporting in the EU, notably affecting housing companies. The German scenario exemplifies an expanded scope, encompassing most of the top 100 German housing companies. Simultaneously, the CSRD brings about clearer and more precise reporting criteria.

The EU Accounting Directive specifies companies subject to CSRD reporting and outlining reporting requirements through the European Sustainability Reporting Standards (ESRS). CSRD aims to make ESRS the EU's mandatory reporting standard, compelling companies to significantly enhance reporting quality. The introduction of an audit requirement aligns sustainability -nonfinancial reporting- reporting with financial reporting scrutiny.

CSRD mandates a reporting obligation on EU taxonomy conformity at the corporate level, necessitating substantial additional efforts for companies. The Sustainable Finance Disclosure Regulation (SFDR) indirectly compels housing companies to consolidate and provide non-financial information. Housing companies must proactively collect pertinent data ahead of impending sustainability disclosure requirements.

The UK applies similar frameworks with little different wording. Main relevance for UK housing companies is in Climate Related Financial Disclosures (CRFD) and Streamlined energy and Carbon Reporting (SECR), fuelled by the UK Green Taxonomy.

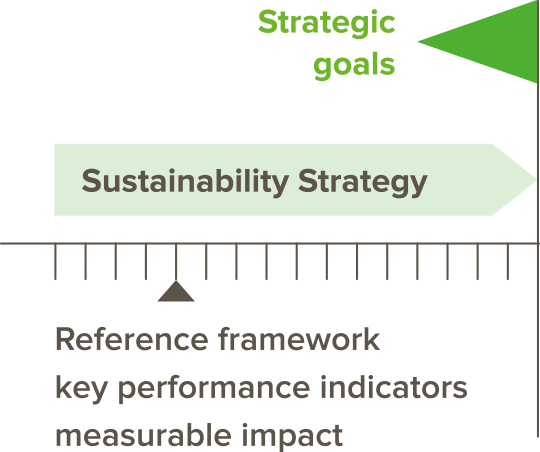

The Corporate Sustainability Strategy is the bridge between strategic goals and operational performance with measurable impact. In line with the sustainability vision and mission, the first step is to define the reference framework. It is also necessary to determine the relevant sustainability definitions, that can be used in a catalogue of goals with key performance indicators. These can then be embedded in the regular business planning cycles.

A social or sustainable finance framework is required to issue a social or sustainable bond.

The framework links the proceeds raised with the bond to tangible and trackable projects demonstrating the sustainability commitment of the issuer. Such a framework must be in alignment with the principles and guidelines from the International Capital Market Association (ICMA) or -in the case of a loan- with the Loan Market Association (LMA).

RITTERWALD supports housing companies with compiling their inaugural Sustainable and Social Bond Framework. Often ESG data derived from the Certified Sustainable Housing Label and materiality analysis supporting the corporate sustainability strategy are used as key input.

As a guiding principle for corporate ESG strategy, a materiality analysis can identify material topics that need to be prioritised.

RITTERWALD supports the compilation of the materiality analysis. Hereby we propose to start with the assessment of the importance of material topic clusters for different stakeholder groups. This can be done by surveys and/or interviews. Afterwards, the relevance of the topic clusters for the housing company from the perspective of all internal and external stakeholder groups is assessed. Finally, the housing company assesses the relevance of the topic clusters for itself by asking several employees.

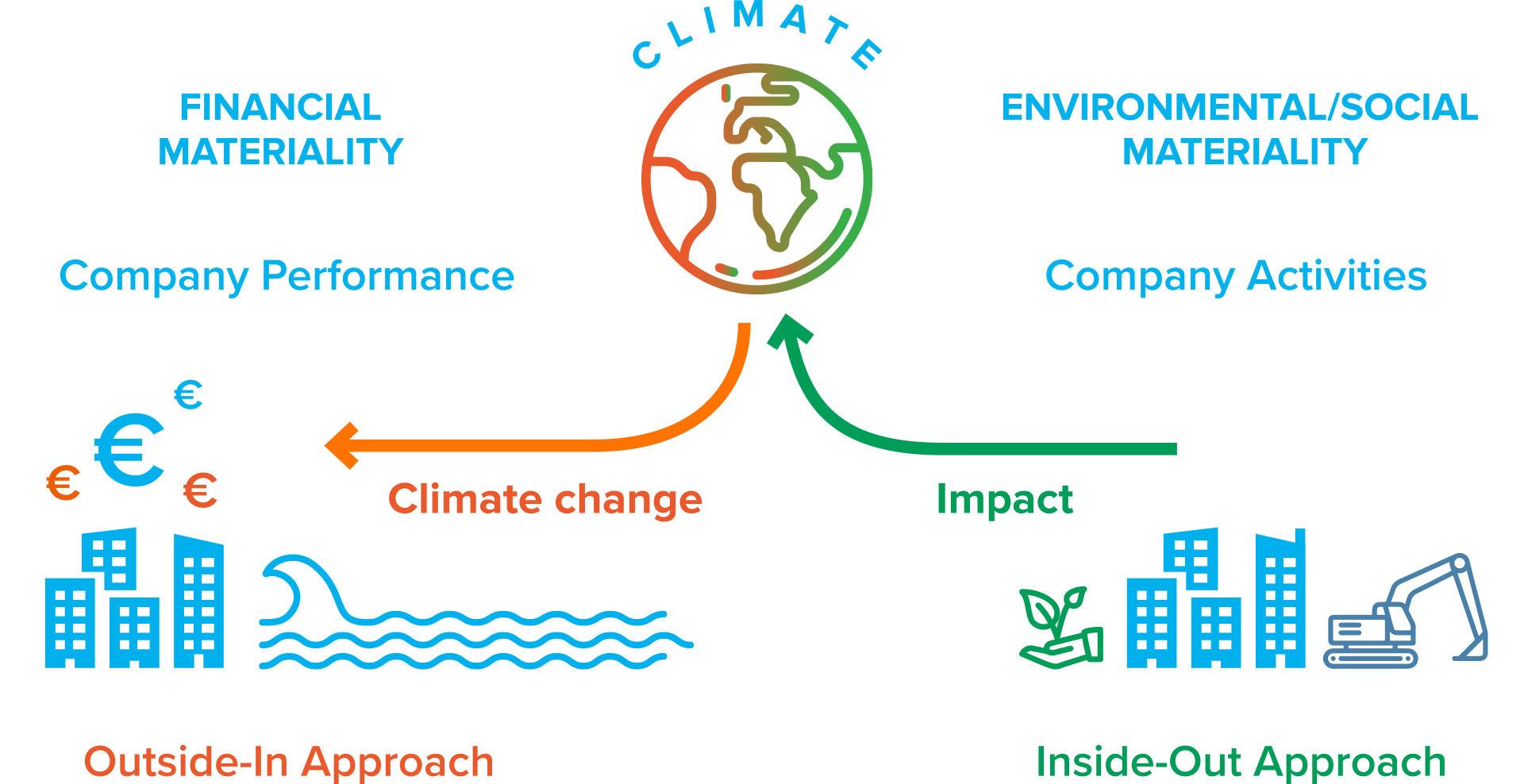

According to the concept of double materiality, companies should report on materiality in two ways:

FINANCIAL MATERIALITY: Companies should reflect the impact of climate change and sustainability developments on the company's financial performance

ENVIRONMENTAL & SOCIAL MATERIALITY: Companies should report on the impact of their activities on the environment and society

With our background of strategic planning and sustainability analysis, RITTERWALD offers a customised approach to housing providers in developing their Corporate Sustainability Strategy:

Analysis of the strategic framework (e.g., by means of PESTEL or SWOT analysis) and identification of suitable frameworks established in the market

Identification of the appropriate strategic reference framework for mapping with sustainability milestones and market standards

Coordinate the catalogue of objectives by conducting a materiality analysis and assigning goals to the identified objective categories

Deriving and prioritising a catalogue of measures to achieve the defined goals and underpinning the strategy with business planning

Development of a roadmap to communicate the short-, medium- and long-term goals